What are the conditions for bidirectional charging – V2G – in France, the UK and Germany? 🇫🇷🇬🇧🇩🇪 ⚡ 🔄 🔌 🔋 🚘

FfE provide an interesting comparison of the different approaches being taken in these three countries.

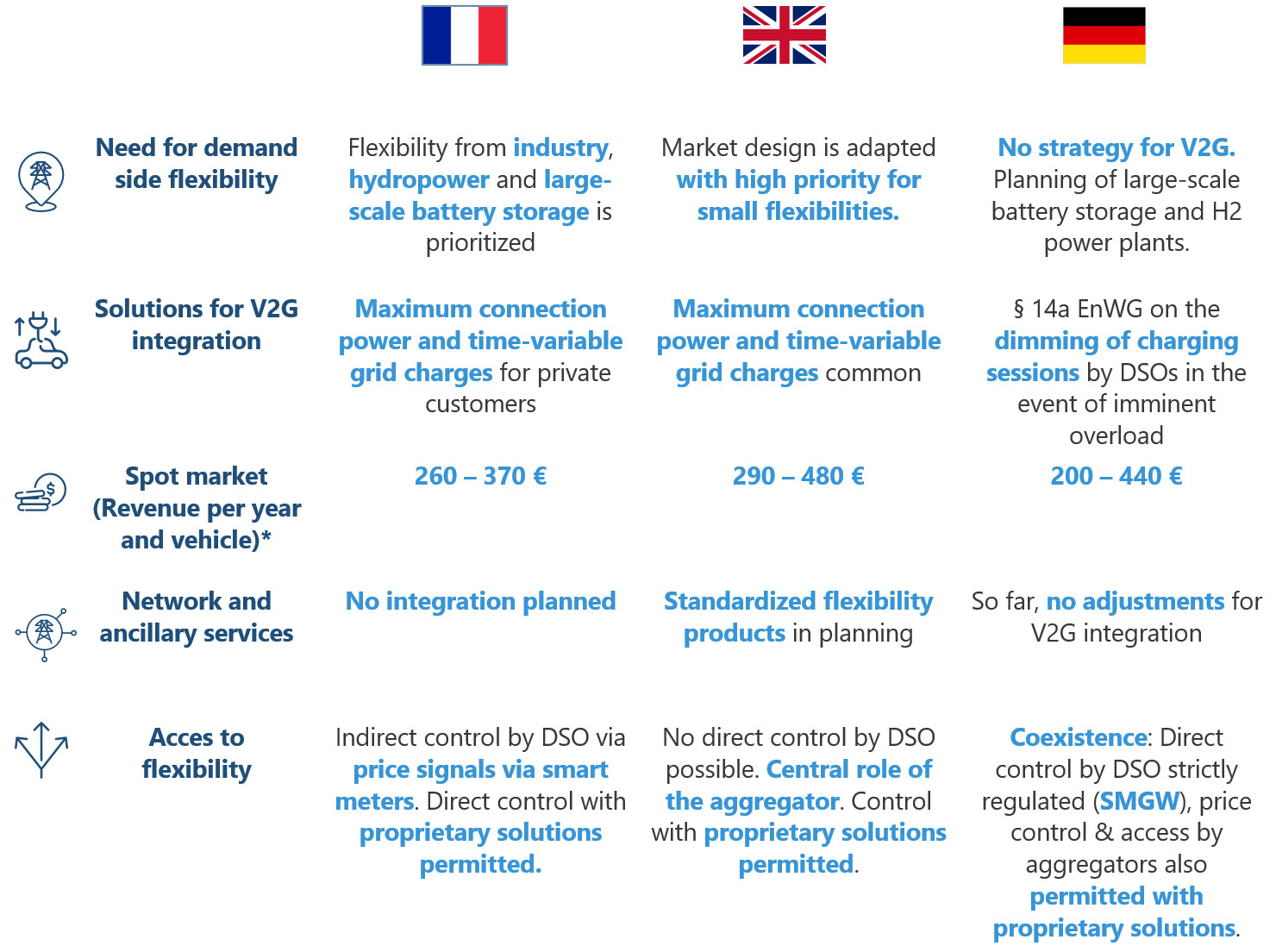

The similarities between the three countries lies in participation in the spot market (all three between €200-480 per year and vehicle in revenues), making this an important factor in the deployment of V2G in Europe. Other services, such as for the local grid, have a much different emphasis. There are also clear differences: e.g. the German particularity of control via the smart meter is not replicable internationally. In France, the first commercialised residential V2G application is underway with Renault R5, but at the same time there is little movement by (transmission/distribution) network operators to exploit this flexibility. In the UK, on the other hand, much work is being done to unlock small-scale flexibility through aggregators and local flexibility markets.

European and EU efforts should (and already do) focus on standardisation, e.g. grid connection requirements (grid codes) and technical interfaces, such as the ISO 15118-20 standard for vehicle-charger communication. Spot market participation is already a common starting point for V2G today. My take-away, also for other European countries working on bidirectional charging: stacking other flexibility services (network, ancillary) should be planned to be compatible with this primary use case.

Looking forward to future work in this series!

https://www.ffe.de/en/publications/publication-of-the-white-paper-on-v2g-integration-in-europe/ (EN)

https://www.ffe.de/veroeffentlichungen/wp-die-v2g-integration-in-europa/ (DE)