One interesting aspect of the electrification of heavy-duty vehicles and buses is how quickly the transition can happen.

The total cost of ownership plays a decisive role. However, the barriers to entry are high, including higher purchase prices for the vehicles and the need for new infrastructure. This is not only a financial barrier, for which business models are emerging, but also a practical barrier in terms of lead times, grid capacity and charger availability. Furthermore, fleets tend to be highly predictable and therefore require reliable charging options.

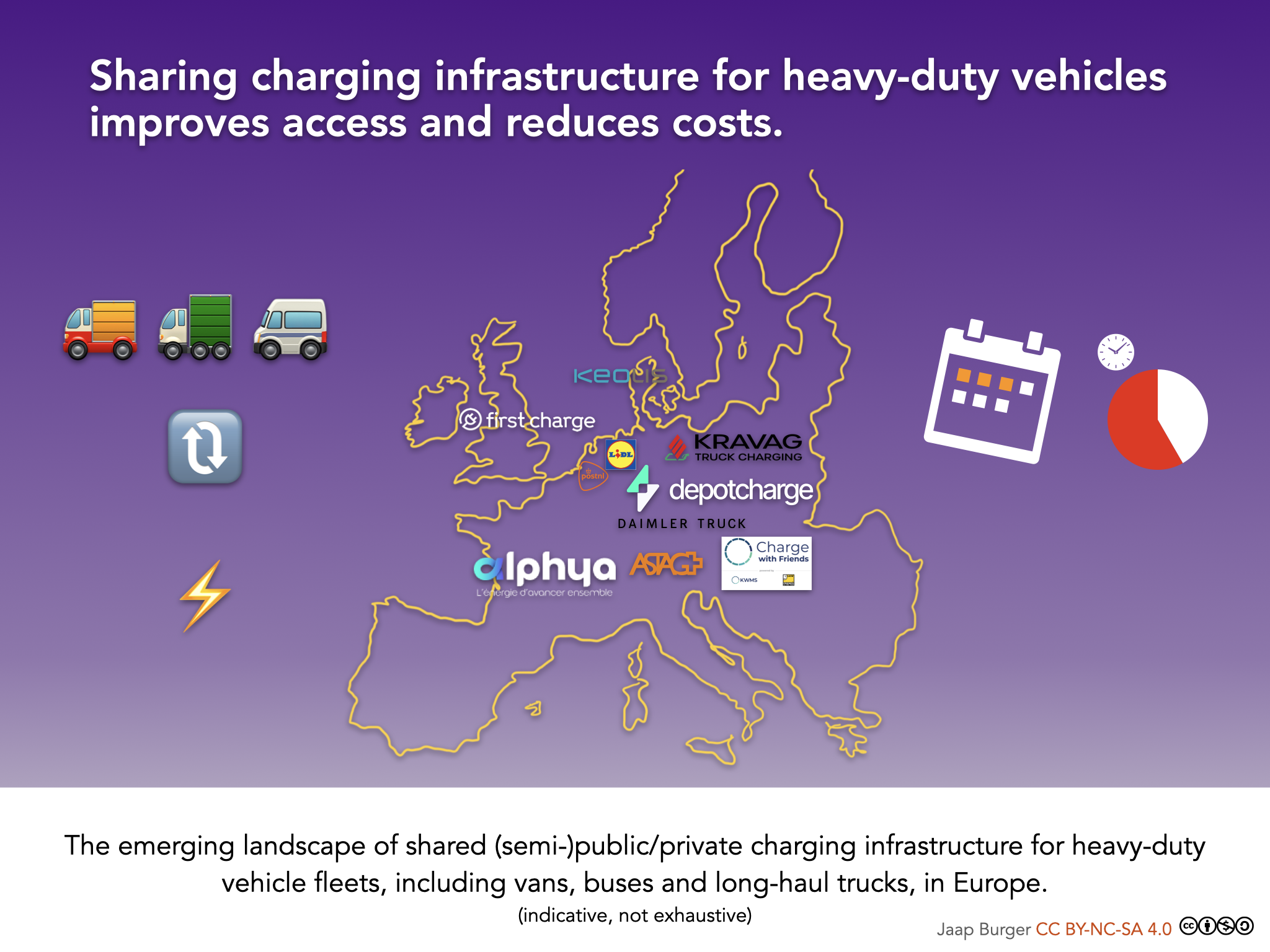

Combined with the focus on total cost of ownership (TCO), where the charging price dominates, this is leading to new business models involving shared semi-public or private charging infrastructure for these fleets.

For example, logistics companies are setting up cooperatives to share depot charging infrastructure, and new platforms are emerging to share infrastructure with selected fleets, with precise time slot agreements. For logistics companies with charging infrastructure, this is an opportunity to improve the return on investment for their charging hubs.

‘Traditional’ public charging operators, who are used to operating in a seller’s market, will have to adapt to secure their share of the lucrative truck charging market. Regardless of the domain, there is a growing need to pass on, for example, locational price incentives from the grid and on-site renewables in order to offer the most competitive prices. The focus will shift towards “access to” models with detailed agreement structures instead of just a margin.

The key growth opportunity lies in the integration (or symbiotic combination) of routing, financing, access, energy, contract, and fleet management.